In fact, it's astoundingly ignorant. Amazingly so.

A) Take the remark about setting a target for five-year yields at 1%. Since the 5-year yield is already under 1%, this wouldn't have accomplished much, would it?

http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldB) Mortgage rates have dropped significantly, yet purchase money mortgage apps are not rising in tandem. We have reached the point at which the mortgage and housing market is insensitive to further drops in rates. This is for several reasons, one of them being that most credit-worthy people already have mortgages, and another being the generally high debt loads among households.

C) Last year's QE2 policy both dropped the dollar and raised inflation rates 3-4%. The result was to tank the economy! Why? Because most Americans live in moderate-income households and inflation rates of 3-4% (where we spent the first half of the year) drop their real incomes, thus cutting their expenditures on non-necessities. This, in turn, tends to cut overall employment.

Some stats:

http://www.bls.gov/news.release/cpi.t04.htmCPI-W 12 month for July (last available) was 4.1%.

http://www.bls.gov/news.release/cpi.t01.htmCPI-U 12 month for July was 3.6% (these have higher incomes than the CPI-W calculation)

US unemployment rate rose from 8.8% in March to 9.1% in August, and over the year (from August 2010 to August 2011) we only gained 360,000 jobs (416,000 NSA).

http://www.bls.gov/webapps/legacy/cpsatab1.htm D) "Reducing the burden of debtors" - it's only doing this for really high income debtors. In fact, delinquency rates for some types of consumer debt are increasing, and don't try to convince me that this is not related to declining real incomes. Interest rates charged to borrowers have several components. The first component is the risk-free comparable rate, and that is currently Treasuries or other gov-guaranteed debt. The next is rate and time risk (what is the chance that rates will rise sharply while the borrower is repaying the loan, thus causing the lender a loss, or in some cases, adverse regulatory or other developments that place the lender's money at risk). Then there is servicing cost - there is an extra interest charge to cover the lender's cost of servicing the loan (collecting payments, performing required auditing/reporting, collecting a defaulted loan). The final is default risk - the chance that the lender will take a loss because the borrower cannot repay the loan. With real "base" interest rates below zero, loan and rate/time risk have far more weight in setting private sector loan rates. A declining economy increases loan risk. Therefore, rate charged to consumers and businesses won't change much more no matter what the Fed does - at this point, rate risk and default risk are quite large factors in the computation. What will change rates charged to consumers will be a better economy.

Facts:

Delinquency rates for residential mortgages have been rising, not falling:

http://www.federalreserve.gov/releases/chargeoff/delallsa.htmLoan rates for consumers have in some cases risen rather than fallen over the last year:

http://www.federalreserve.gov/releases/g19/current/g19.htmNote that credit card rates have fallen, but the reason is not a change in Fed or Treasury rates, but a big drop in chargeoffs, which control credit card rates more than anyone wants to believe:

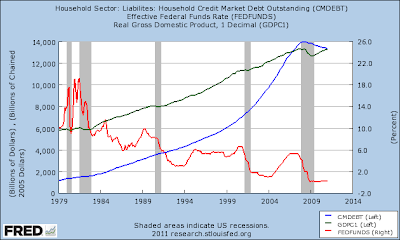

http://www.federalreserve.gov/releases/chargeoff/chgallsa.htmLast, the entire article seems to ignore the blindingly obvious reality that Americans have stunningly high levels of household debt, so the economy can't respond to changes in interest rates the way it used to. This graph shows GDP in green, household debt in blue and the effective Fed funds rate in red:

So, the article is advocating a policy that is only good for rich people, and even more entertainingly, advocating a policy that has already been tried and has reached the end of whatever good it can do.