| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

| KansasVoter

|

Wed Jun-09-10 11:31 PM Original message |

| Will the day come when if your 401K is too valuable, you lose Social Security? |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Wed Jun-09-10 11:32 PM Response to Original message |

| 1. SS can't "go broke". |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Wed Jun-09-10 11:35 PM Response to Reply #1 |

| 4. If they keep borrowing from it it can. Look it up! |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Wed Jun-09-10 11:36 PM Response to Reply #4 |

| 7. no, it can't. there's nothing to look up. |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Wed Jun-09-10 11:38 PM Response to Reply #7 |

| 9. LOL....you are full of information. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:04 AM Response to Reply #9 |

| 21. you've provided none yourself, plus you called me an "idiot" without any provocation |

| Printer Friendly | Permalink | | Top |

| dionysus

|

Thu Jun-10-10 10:04 AM Response to Reply #21 |

| 123. wow, a post of yours i am in agreement with. good information comrade Bell. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Wed Jun-09-10 11:52 PM Response to Reply #7 |

| 19. SS is also cashflow negatvie (early because of recession) |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:07 AM Response to Reply #19 |

| 22. no, the trust fund is cash-negative -- if you don't count interest payments, which continue |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:11 AM Response to Reply #22 |

| 24. Because it is going negative faster than anticipated. I ins't a HUGE problem but it exists |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:20 AM Response to Reply #24 |

| 30. uh, "faster than anticipated" -- because we're in a major recession. the fact is, with the interest |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:22 AM Response to Reply #30 |

| 33. I never used the strawman term "crisis" however I don't consider a 25% benefit cut in 30 years to |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:46 AM Response to Reply #33 |

| 46. As I've repeatedly told you, it's not a cut at all in terms of today's benefit levels. It would |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:52 AM Response to Reply #46 |

| 49. Wrong. Wrong. Wrong. Saying it over and over doesn't make it true. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:12 AM Response to Reply #49 |

| 53. You are completely mistaken. Let's check. Average monthly SS check (all workers) in |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:25 AM Response to Reply #53 |

| 57. That was only because the wages for THOSE workers rose faster than inflation. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:03 AM Response to Reply #57 |

| 68. Let me remind you of your initial claim: |

| Printer Friendly | Permalink | | Top |

| Lasher

|

Thu Jun-10-10 06:03 AM Response to Reply #68 |

| 103. Guess not. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 02:43 AM Response to Reply #57 |

| 85. You are right. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 03:02 AM Response to Reply #85 |

| 88. Yeah it is a pretty well understood concept.... |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 03:49 AM Response to Reply #88 |

| 90. The poster said I was right, not you. The COLA has nothing to do with anything. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 04:32 PM Response to Reply #90 |

| 130. I don't think my very, very elderly mother's checks have risen except for inflation. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 04:31 PM Response to Reply #88 |

| 129. Yes. I am on Social Security, and I worked half of last year, so my SS |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 03:40 AM Response to Reply #85 |

| 89. social security benefits are only partially based on your earnings. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 04:38 PM Response to Reply #89 |

| 131. In other words, the scheduled benefits are based on projected rises in |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 12:28 AM Response to Reply #24 |

| 38. Change our trade policy and bring the jobs back to the U.S. and the |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:33 AM Response to Reply #38 |

| 40. It will help but it won't solve the whole problem. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:50 AM Response to Reply #40 |

| 48. There is no problem except the incessant pounding of the propaganda. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:55 AM Response to Reply #48 |

| 51. I haven't once used the term "crisis". |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:19 AM Response to Reply #51 |

| 54. "Doing nothing" FOR AT LEAST 25 YEARS is in fact the BEST OPTION. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:31 AM Response to Reply #54 |

| 61. "Twenty-five years down the road maybe we might have to raise SS taxes a dollar a week in real terms |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:38 AM Response to Reply #61 |

| 63. My generation (and the previous one, and a couple of ones after us) |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:45 AM Response to Reply #63 |

| 65. It wasn't enough. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:10 AM Response to Reply #65 |

| 70. the entire "let's put trillions in the trust fund to pay for retirements 30 years in the future" was |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:23 AM Response to Reply #65 |

| 74. it wasn't? then why did ronnie say it was? |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:29 AM Response to Reply #74 |

| 75. It was close. Less than 0.5% difference between projected funding and projected costs. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:32 AM Response to Reply #75 |

| 77. Look, I've already disproved every claim you've made. I've actually |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:36 AM Response to Reply #77 |

| 79. The trustee reports are based on the agregate. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:43 AM Response to Reply #79 |

| 84. lol. "the aggregate". this must be why the average benefit rose 29% |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:49 AM Response to Reply #84 |

| 87. Because a retiree in 2010 worked the 3 decades prior. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 04:18 AM Response to Reply #87 |

| 92. Let me again remind you of your initial claim, the one you've done your best to obfuscate with |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 06:28 AM Response to Reply #75 |

| 106. it's STILL all projections. you act as if they were a fait accompli, a completely |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 04:46 PM Response to Reply #61 |

| 133. No matter what you do, these costs will be passed on to the next generation. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 02:46 AM Response to Reply #40 |

| 86. People are retiring early because they can't get jobs. I know. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 12:27 AM Response to Reply #19 |

| 36. Outsourced jobs an imported products = high unemployment = low tax revenues |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 05:51 AM Response to Reply #36 |

| 102. agree with that, except for the balanced budget part. add wage increases to your picture. |

| Printer Friendly | Permalink | | Top |

| Incitatus

|

Wed Jun-09-10 11:40 PM Response to Reply #4 |

| 13. I thought they were only borrowing the surplus. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Wed Jun-09-10 11:45 PM Response to Reply #13 |

| 17. "Payments might diminish " |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:16 AM Response to Reply #17 |

| 28. the point at which that will happen is 30 years in the future, according to current projections. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:20 AM Response to Reply #28 |

| 31. No I agree 100% it isn't massive. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:21 AM Response to Reply #31 |

| 32. your fixes aren't currently needed. there is no "compounding" - the money is just |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:25 AM Response to Reply #32 |

| 35. Then the trust fund will run out early (2037) and benefits will be cut 25%. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:35 AM Response to Reply #35 |

| 42. you have no idea what will be happening in 2037. last year, the number was different. it's been |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:45 AM Response to Reply #42 |

| 45. No it doesn't. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:54 AM Response to Reply #45 |

| 50. you're mistaken. the COLA is completely different from the benefits schedule. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:58 AM Response to Reply #50 |

| 52. "which rise in real terms." |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:23 AM Response to Reply #52 |

| 56. The projections you're taking as gospel are indeed based on that assumption |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:40 AM Response to Reply #56 |

| 64. Your misunderstanding. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:03 AM Response to Reply #64 |

| 69. No, yours: |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:20 AM Response to Reply #69 |

| 73. Your social security year1 benefit is based on your wages. Period. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:30 AM Response to Reply #73 |

| 76. no, it isn't. it's based on your wages AND THE BENEFITS SCHEDULE. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:38 AM Response to Reply #76 |

| 81. Nope that didn't say the schedule is going up. |

| Printer Friendly | Permalink | | Top |

| JDPriestly

|

Thu Jun-10-10 12:34 AM Response to Reply #31 |

| 41. The average Social Security benefit in December 2009 was, I read, |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:40 AM Response to Reply #41 |

| 43. I think you misunderstand. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:29 AM Response to Reply #43 |

| 60. your list is unnecessary, misinformed, and mostly pernicious. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:35 AM Response to Reply #60 |

| 62. "not to mention that social security benefits have been taxed since 1983, did you not get the memo?" |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:14 AM Response to Reply #62 |

| 71. You think "high net worth individuals" have some kind of exemption from income taxes? |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:41 AM Response to Reply #71 |

| 83. Nope it isn't taxed at full tax rate. There is an offset, has been since they started taxing it. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 04:40 AM Response to Reply #83 |

| 96. SO WHAT? They DON'T GET 85% of the benefits they paid for OVER A WORKING LIFE. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:42 AM Response to Reply #41 |

| 44. The poster is misinformed about that "25%". It's 25% of SCHEDULED benefits. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:49 AM Response to Reply #44 |

| 47. Wrong. You are 100% wrong and repeating it over and over doesn't change it. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 01:21 AM Response to Reply #47 |

| 55. Hogwash. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:27 AM Response to Reply #55 |

| 58. Benefit amount is based on YOUR WAGES. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:15 AM Response to Reply #58 |

| 72. hogwash. period. |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:32 AM Response to Reply #72 |

| 78. CBO is projecting WAGES will rise faster than inflation. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 02:36 AM Response to Reply #78 |

| 80. Your benefits at year one are based on your lifetime earnings AND THE SCHEDULE OF BENEFITS |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 02:39 AM Response to Reply #80 |

| 82. No trustee report project REAL WAGE increases. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 04:52 AM Response to Reply #82 |

| 98. Every Trustees' report projects REAL wage increases. Try reading one. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:09 AM Response to Reply #13 |

| 23. correct. the posters are confusing the drawing down of the trust fund -- |

| Printer Friendly | Permalink | | Top |

| girl gone mad

|

Thu Jun-10-10 12:14 AM Response to Reply #4 |

| 25. No. |

| Printer Friendly | Permalink | | Top |

| Vickers

|

Wed Jun-09-10 11:32 PM Response to Original message |

| 2. That thought has crossed my mind, and once again I will be penalized |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Wed Jun-09-10 11:35 PM Response to Reply #2 |

| 3. So true! Just like paying your mortgage on time. |

| Printer Friendly | Permalink | | Top |

| WinkyDink

|

Thu Jun-10-10 07:20 AM Response to Reply #2 |

| 113. In schools, it's the kids whose parents lived high & in debt who gwe the scholarships. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:22 AM Response to Reply #113 |

| 115. gwe? get? |

| Printer Friendly | Permalink | | Top |

| Kookaburra

|

Wed Jun-09-10 11:36 PM Response to Original message |

| 5. Sorry -- |

| Printer Friendly | Permalink | | Top |

| awoke_in_2003

|

Thu Jun-10-10 12:29 AM Response to Reply #5 |

| 39. yeah, they lost me there. nt |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Wed Jun-09-10 11:36 PM Response to Original message |

| 6. I fear it. |

| Printer Friendly | Permalink | | Top |

| Hassin Bin Sober

|

Wed Jun-09-10 11:44 PM Response to Reply #6 |

| 16. Buy more BP stock and you won't have a problem |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 09:47 AM Response to Reply #16 |

| 121. BURN! |

| Printer Friendly | Permalink | | Top |

| Hassin Bin Sober

|

Thu Jun-10-10 10:15 AM Response to Reply #121 |

| 125. How much worse can it get? |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 10:19 AM Response to Reply #125 |

| 126. Yeah I am still watching it but... |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Wed Jun-09-10 11:37 PM Response to Original message |

| 8. only if you allow it to happen by buying into the scare stories -- like the one you just repeated, |

| Printer Friendly | Permalink | | Top |

| Name removed

|

Wed Jun-09-10 11:38 PM Response to Reply #8 |

| 11. Deleted message |

| Sherman A1

|

Thu Jun-10-10 04:09 AM Original message |

| Thanks! |

| Printer Friendly | Permalink | | Top |

| Sherman A1

|

Thu Jun-10-10 04:09 AM Response to Reply #8 |

| 91. Thanks! |

| Printer Friendly | Permalink | | Top |

| The_Casual_Observer

|

Wed Jun-09-10 11:38 PM Response to Original message |

| 10. The number of 401ks that go over a million would be so small that |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Wed Jun-09-10 11:39 PM Response to Reply #10 |

| 12. Just an example number. Could be $500,000 |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Wed Jun-09-10 11:47 PM Response to Reply #10 |

| 18. Are you account for inflation. |

| Printer Friendly | Permalink | | Top |

| DURHAM D

|

Wed Jun-09-10 11:41 PM Response to Original message |

| 14. No. |

| Printer Friendly | Permalink | | Top |

| Incitatus

|

Wed Jun-09-10 11:42 PM Response to Reply #14 |

| 15. Obama said SS will go broke? |

| Printer Friendly | Permalink | | Top |

| DURHAM D

|

Wed Jun-09-10 11:54 PM Response to Reply #15 |

| 20. Link? |

| Printer Friendly | Permalink | | Top |

| Stardust

|

Thu Jun-10-10 12:15 AM Response to Original message |

| 26. Frankly, if your 401K is worth a million, why would you care? |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 12:27 AM Response to Reply #26 |

| 37. Inflation. |

| Printer Friendly | Permalink | | Top |

| flamingdem

|

Thu Jun-10-10 01:28 AM Response to Reply #37 |

| 59. Shouldn't inflation be offset by gains in the market? nt |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 01:47 AM Response to Reply #59 |

| 67. Gains in the market is likely how one gets a million dollar 401K. |

| Printer Friendly | Permalink | | Top |

| happy_liberal

|

Thu Jun-10-10 12:15 AM Response to Original message |

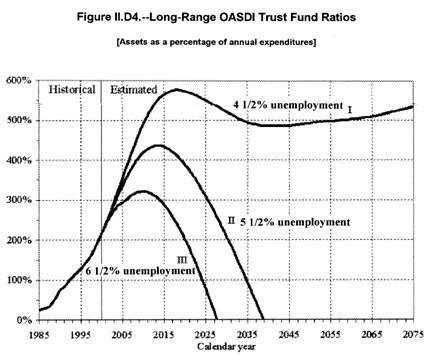

| 27. I hope this chart isn't accurate... |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 12:25 AM Response to Reply #27 |

| 34. that chart is a bunch of shit. unless you believe it's legitimate to represent *projected* |

| Printer Friendly | Permalink | | Top |

| Oregone

|

Thu Jun-10-10 12:19 AM Response to Original message |

| 29. No |

| Printer Friendly | Permalink | | Top |

| SoCalDem

|

Thu Jun-10-10 01:46 AM Response to Original message |

| 66. unlikely.. even in the good-times, most people's 401-ks were worth less than 50k |

| Printer Friendly | Permalink | | Top |

| spinbaby

|

Thu Jun-10-10 04:22 AM Response to Reply #66 |

| 94. A good point |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 04:22 AM Response to Original message |

| 93. If your a millionaire, you don't need social security |

| Printer Friendly | Permalink | | Top |

| lamp_shade

|

Thu Jun-10-10 04:31 AM Response to Reply #93 |

| 95. +1 I know a bazillionaire who "laughs" at the fact that she gets a SS check every month. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 04:54 AM Response to Reply #95 |

| 99. who cares? she got what every other retiree who paid in what she did got. |

| Printer Friendly | Permalink | | Top |

| WinkyDink

|

Thu Jun-10-10 07:22 AM Response to Reply #99 |

| 114. The "Who cares?" part is what kind of nation are we? WHO SAYS THE POOREST MUST PAY FROM THEIR |

| Printer Friendly | Permalink | | Top |

| Lasher

|

Thu Jun-10-10 05:32 AM Response to Reply #93 |

| 100. The Department of Defense doesn't have a trust fund at all. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 05:41 AM Response to Reply #100 |

| 101. :>) good point. & if we project their spending 75 years into the future, it consumes the entire |

| Printer Friendly | Permalink | | Top |

| Lasher

|

Thu Jun-10-10 06:21 AM Response to Reply #101 |

| 104. You are pickin' up what I'm layin' down. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 06:23 AM Response to Reply #104 |

| 105. ah, the trail of tears & broken promises. |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Thu Jun-10-10 07:03 AM Response to Reply #93 |

| 107. Bullshit! They paid in, they deserve it back! |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 07:12 AM Response to Reply #107 |

| 109. Its a payroll tax |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:19 AM Response to Reply #109 |

| 112. Millionaires make their money from capital, not from wages. |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 07:30 AM Response to Reply #112 |

| 117. why do you care? |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:32 AM Response to Reply #117 |

| 119. THERE IS NO SOCIAL SECURITY "PROBLEM" EXCEPT FOR THOSE WHO WANT TO DESTROY IT. |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 01:50 PM Response to Reply #119 |

| 128. Even if your right |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Thu Jun-10-10 09:55 AM Response to Reply #117 |

| 122. Millionare is not as rich as you think especially not in the future. |

| Printer Friendly | Permalink | | Top |

| Lasher

|

Thu Jun-10-10 10:54 AM Response to Reply #122 |

| 127. This is a good point. |

| Printer Friendly | Permalink | | Top |

| KansasVoter

|

Thu Jun-10-10 09:13 AM Response to Reply #109 |

| 120. They already are. They pay MOST of the taxes. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:10 AM Response to Reply #93 |

| 108. they currently might "give back" as much of 85% of their earned benefits. |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 07:13 AM Response to Reply #108 |

| 110. then we shouldn't do that. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:18 AM Response to Reply #110 |

| 111. there's no requirement we turn social security into a welfare program, either. |

| Printer Friendly | Permalink | | Top |

| yodoobo

|

Thu Jun-10-10 07:27 AM Response to Reply #111 |

| 116. But there is a requirement to fix a system that is going broke. |

| Printer Friendly | Permalink | | Top |

| Hannah Bell

|

Thu Jun-10-10 07:31 AM Response to Reply #116 |

| 118. Social security isn't "going broke," so what system are you talking about? |

| Printer Friendly | Permalink | | Top |

| LiberalEsto

|

Thu Jun-10-10 04:46 AM Response to Original message |

| 97. What 401K? nt |

| Printer Friendly | Permalink | | Top |

| Skidmore

|

Thu Jun-10-10 10:04 AM Response to Original message |

| 124. 401Ks and retirement funds have become a joke since many |

| Printer Friendly | Permalink | | Top |

| Common Sense Party

|

Thu Jun-10-10 04:42 PM Response to Reply #124 |

| 132. How have you been "forced into participating" in any plans as a condition |

| Printer Friendly | Permalink | | Top |

| Change Happens

|

Thu Jun-10-10 05:19 PM Response to Original message |

| 134. Yes... |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Sun May 05th 2024, 09:57 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC