|

There are two aspects to an economy. There's the support economy, which basically is all the jobs that support a region (however you define that region), such as restaurants, local businesses. They sell to the people in the region. Then there's the base economy, which is the business that brings money into a region from outside of it. The base economy is what gives people money to support the support economy.

Since Reagan, the US has been a debtor nation, meaning we import more goods than we export. That means our base economy is not bringing in enough money. The inevitable result of that, long term, is that our money becomes worth less and less compared to the rest of the world's money, and our jobs slowly evaporate.

The biggest cause of this problem is Reagonomics. Reagan believed--for outdated economic reasons--that if you give the wealthiest industries more money and give them an incentive to invest that money, they will spend it on creating more jobs. The problem with the theory is obvious and simple--industry doesn't make a product because they have money to make it, they make a product because there is a market to buy it. GM wasn't going to make more cars and put more people back to work if no one was buying their cars in the first place. Instead, they invested the money by buying up markets that already were making money--parts, tires, smaller car makers, etc. This created no new jobs, since they were just buying existing jobs. It only shifted those jobs from smaller ownership to larger ownership, and in the process reduced the number of employers.

So take the tax cuts that gave more money to the wealthy, giving them an unfair advantage in business competition against smaller businesses who did not get as much money back, and take the shrinking employer base from larger businesses buying smaller businesses (those who remember the 80s know that the big words then on Wall Street were merger and takeover), and you have middle and lower economic classes making less money, therefore starting fewer businesses, therefore not contributing to the base economy.

Clinton--who should be worshipped by progressives, not condemned--reversed Reaganomics. His raised taxes marginally on the wealthiest, and lowered them on the middle and lower classes. Instantly, the market responded. Larger companies no longer found it profitable to hold monopolies just for the sake of investing their extra cash, because there was no extra cash. So they either closed their marginal businesses, or sold them, or let them spin off. Since there was still a market for whatever these companies produced, the middle classes with their new competitive buying power bought them up, or ran them as employee investors. Key words on Wall Street during Clinton were spinoff, and startup. Wages started going up, poverty shrank to as low as one can expect it, and the deficit came down because finally there was enough of a base economy for tax revenues to finally outstrip the requirement to spend and borrow.

Bush reversed that, and we started down the Reagan path again. Obama's stimulus package, while having a lot of Clintonomics in it, still carried a little too much trickle-down to really reverse things, but he did stop the bleeding. Right now we are tottering on an edge, seeing if the weight of the economy will pull us back to safety or pull us over the edge. Obama halted the problem, but whether he did enough for the solution remains to be seen. He knows this, I think, which is why he's talked about additional stimulus bills. On the other hand, he's still too much a believer in the Republican tax-cuts-will-stimulate-the-economy mentality. Long term tax cuts that target the middle and lower classes while making up for the shortfall through taxation of the wealthiest, and more importantly of corporate wealth, would do what he wants, but that's the part he's not as clear on.

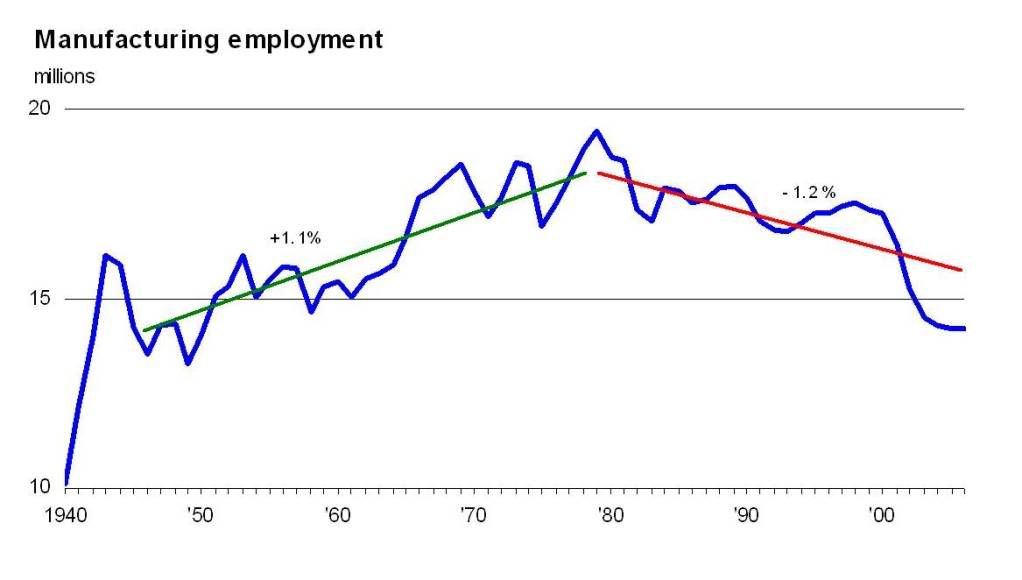

Anyway, I agree with you that bringing back the manufacturing base would create jobs. That is a big part of the base economy, as is agriculture, technological research and innovation, and anything we can do better than someone else. That's what they pay us for. The best way to bring that part of our economy back, though, is to tax the wealthy. Make it less profitable for them to make products overseas, and people will start making them here. I have no problem with NAFTA, because if we taxed income (personal and business) progressively, smaller businesses would be stimulated, and larger businesses would be curtailed, and manufacturing would return. Let China keep making cheap stuff we don't want to make anyway, and let us keep buying it cheap. That helps China and us. But we have to make what we make best over here, and that's where our economy is shot.

Under Clinton, we saw an incredible tech boom, not because people were suddenly inventing stuff, but because there was suddenly enough middle-class money to invest in smaller markets, so people with ideas could make money off the ideas. Reagan and W killed that aspect of the economy. That's what we need to bring back. And the good part is that it's simple to bring back--just realign our tax structure, and the money is there, and suddenly our brilliant thinkers will create a fortune on green technology, the next generation of computers, or whatever. Tax cuts are relative--you have to tax the wealthiest most heavily to make the market more competitive for those just starting up. That's the biggest mistake Obama has made so far.

Anyway, that's how I'd fix the economy. :)

Excellent post, btw. My long ramble wasn't a contradiction, just thoughts inspired by your point. Well done, and thanks. :thumbsup:

|