| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

| SOCALS

|

Tue Dec-22-09 04:32 PM Original message |

| Current average credit score in US? |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Tue Dec-22-09 04:40 PM Response to Original message |

| 1. Credit scores are getting to be totally irrelevant |

| Printer Friendly | Permalink | | Top |

| SOCALS

|

Tue Dec-22-09 04:43 PM Response to Reply #1 |

| 2. Do you avoid credit cards and loans on purpose? |

| Printer Friendly | Permalink | | Top |

| blondeatlast

|

Tue Dec-22-09 04:46 PM Response to Reply #2 |

| 3. Does there need to be a point? Maybe they just choose to live that way, yanno, like your |

| Printer Friendly | Permalink | | Top |

| BR_Parkway

|

Tue Dec-22-09 04:52 PM Response to Reply #2 |

| 4. There's plenty of us who live without debt - it makes it nice to have |

| Printer Friendly | Permalink | | Top |

| SOCALS

|

Tue Dec-22-09 04:56 PM Response to Reply #4 |

| 5. How do you buy a car |

| Printer Friendly | Permalink | | Top |

| BR_Parkway

|

Wed Dec-23-09 03:57 PM Response to Reply #5 |

| 15. I make the car "payments" to my savings account, then write a check |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Tue Dec-22-09 04:56 PM Response to Reply #2 |

| 6. I was raised by Depression babies, allergic to debt |

| Printer Friendly | Permalink | | Top |

| Godhumor

|

Tue Dec-22-09 05:03 PM Response to Original message |

| 7. Don't have the numbers offhand, but, yes, recessions usually cause avg. scores to go down |

| Printer Friendly | Permalink | | Top |

| SOCALS

|

Tue Dec-22-09 05:05 PM Response to Reply #7 |

| 8. So if the difference between my score and the average increases |

| Printer Friendly | Permalink | | Top |

| Godhumor

|

Tue Dec-22-09 05:28 PM Response to Reply #8 |

| 9. Usually what happens is that a bank or lender will incentivize people... |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Tue Dec-22-09 05:29 PM Response to Original message |

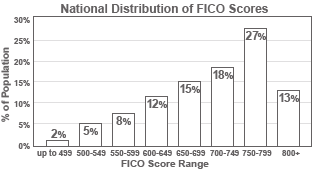

| 10. Fair Issaic (company that manages FICO score) says median hasn't changed and is still 724 |

| Printer Friendly | Permalink | | Top |

| SOCALS

|

Tue Dec-22-09 05:37 PM Response to Reply #10 |

| 12. So do they care about the average at all? |

| Printer Friendly | Permalink | | Top |

| Statistical

|

Tue Dec-22-09 05:41 PM Response to Reply #12 |

| 13. Not really. |

| Printer Friendly | Permalink | | Top |

| ORDagnabbit

|

Tue Dec-22-09 05:34 PM Response to Original message |

| 11. its a game with made up number and rules.. |

| Printer Friendly | Permalink | | Top |

| goldcanyonaz

|

Tue Dec-22-09 05:41 PM Response to Original message |

| 14. I wish they would get rid of credit scoring. |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Mon May 06th 2024, 05:33 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC