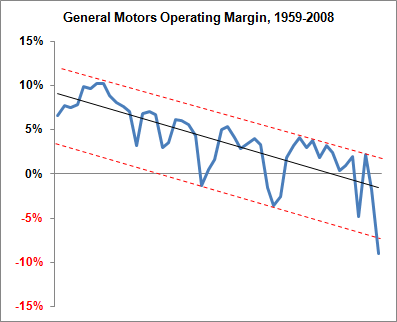

GM's Problems are 50 Years in the MakingLet's take something of a 30,000-foot view on the condition of General Motors. The chart below details GM's operating margin -- its profits divided into its revenues -- over the past 50 years:

haven't provided the dates on the chart because they aren't important. The auto business is highly cyclical because consumers are buying expensive assets that last for years at a time. Nobody ever really has to buy a new car (they can buy a used one if their car breaks down), and therefore consumers are willing to hold on to their existing vehicles and wait out economic slumps. You can't do that with, say, a loaf of bread, or even something like a cellphone, which has a much shorter lifespan.

But you knew all of that already. The remarkable thing is that, once you account for the economic cycles, the trend for GM is exceptionally steady -- an exceptionally steady trend downward. There were still bad times thirty years ago -- but they weren't bad enough to threaten GM's survival, and conversely, the good times were much better. These are General Motors' operating margins by decade:

Average Annual Operating Margin, General Motors

1960s: 8.7%

1970s: 5.5%

1980s: 3.0%

1990s: 1.3%*

2000s: -0.5%

* Excludes one-time $20 billion accounting charge for retiree health benefits in 1992.

If I were an alien beaming down from Rigel-3 looking at this pattern -- an alien with an MBA degree -- my first guess is that it would reflect some sort of systemic problem, some chronic imbalance that magnified over time. Something, in other words, like the costs of GM's retiree pension and health care programs. It's difficult to get a precise figure on these so-called legacy costs, but they averaged about $7 billion per year between 1993 and 2007 and are probably at least $10 billion per year now. Considering that GM has never made as much as $10 billion in profit in a year and that its entire operating lossses in 2008 were $13.8 billion, you can see why this is a significant problem.

Of course, GM benefited by promising its employees access to lucrative retirement programs -- it benefited by being able to pay less to those employees in the form of salary. But whereas the benefits to GM came long ago, the costs come now. This, indeed, is the entire crux of the problem, so cogently explained by this Washington Post article from 2005:

GM began its slide down the slippery slope in 1950, when it began picking up costs for medical insurance, pensions and retiree benefits. There was huge risk to GM in taking on these obligations -- but that didn't show up as a cost or balance-sheet liability. By 1973, the UAW says, GM was paying the entire health insurance bill for its employees, survivors and retirees, and had agreed to "30 and out" early retirement that granted workers full pensions after 30 years on the job, regardless of age.

These problems began to surface about 15 years ago because regulators changed the accounting rules. In 1992, GM says, it took a $20 billion non-cash charge to recognize pension obligations. Evolving rules then put OPEB on the balance sheet. Now, these obligations -- call it a combined $170 billion for U.S. operations -- are fully visible. And out-of-pocket costs for health care are eating GM alive.

More (plus insightful commentary in the thread):

http://www.fivethirtyeight.com/2009/03/gms-problems-are-50-years-in-making.html