| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion: Presidential (Through Nov 2009) |

|

| unlawflcombatnt

|

Sat Mar-25-06 05:15 PM Original message |

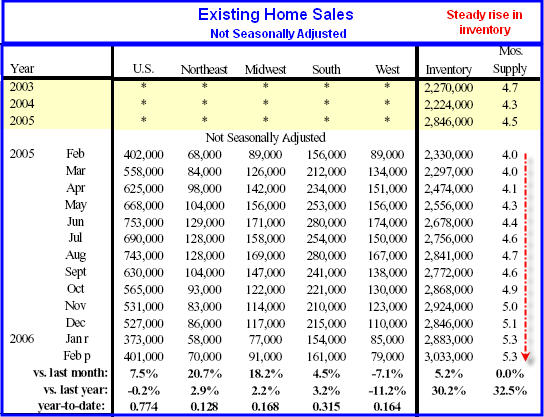

| Housing Market Declining Rapidly |

| Printer Friendly | Permalink | | Top |

| benburch

|

Sat Mar-25-06 05:18 PM Response to Original message |

| 1. You cannot burn the candle at both ends forever. |

| Printer Friendly | Permalink | | Top |

| chaumont58

|

Sat Mar-25-06 05:38 PM Response to Original message |

| 2. To show how crazy it has been |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Sat Mar-25-06 07:15 PM Response to Reply #2 |

| 10. The one I bought in a bad neighborhood |

| Printer Friendly | Permalink | | Top |

| cornermouse

|

Sat Mar-25-06 05:38 PM Response to Original message |

| 3. What, primarily, do the markjority of people tend to invest |

| Printer Friendly | Permalink | | Top |

| msongs

|

Sat Mar-25-06 05:54 PM Response to Reply #3 |

| 5. the did you know that a house you live in is NOT an asset? nt |

| Printer Friendly | Permalink | | Top |

| cornermouse

|

Sat Mar-25-06 07:12 PM Response to Reply #5 |

| 8. The house you live in is a long term investment. |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Sat Mar-25-06 07:19 PM Response to Reply #8 |

| 11. If you can buy for what you pay in rent, then buy |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sat Mar-25-06 07:32 PM Response to Reply #11 |

| 12. Rent vs. Mortgage |

| Printer Friendly | Permalink | | Top |

| cornermouse

|

Sat Mar-25-06 08:12 PM Response to Reply #12 |

| 14. Okay. |

| Printer Friendly | Permalink | | Top |

| Jamison

|

Sun Mar-26-06 02:26 PM Response to Reply #14 |

| 39. No thanks to home-ownership, I'll continue to rent. |

| Printer Friendly | Permalink | | Top |

| Bush_Eats_Beef

|

Sat Mar-25-06 08:20 PM Response to Reply #12 |

| 16. It's true in the Bay Area too. |

| Printer Friendly | Permalink | | Top |

| Gormy Cuss

|

Sat Mar-25-06 09:06 PM Response to Reply #16 |

| 20. Yes, it's always worth checking those calculators in high cost markets |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Sat Mar-25-06 08:20 PM Response to Reply #11 |

| 17. Don't forget to factor in property taxes. Those have been rising a lot |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Sun Mar-26-06 12:25 AM Response to Reply #17 |

| 25. I should have specified the type of mortgage payment |

| Printer Friendly | Permalink | | Top |

| sendero

|

Sun Mar-26-06 02:56 PM Response to Reply #8 |

| 41. Buying a home.. |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sat Mar-25-06 07:13 PM Response to Reply #3 |

| 9. Gold |

| Printer Friendly | Permalink | | Top |

| IndyOp

|

Sun Mar-26-06 10:04 AM Response to Reply #9 |

| 31. A really naive question about gold -- |

| Printer Friendly | Permalink | | Top |

| Gormy Cuss

|

Sat Mar-25-06 05:47 PM Response to Original message |

| 4. It drives me crazy when there is focus on only the most recent month |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sat Mar-25-06 07:45 PM Response to Reply #4 |

| 13. Long Term |

| Printer Friendly | Permalink | | Top |

| BlueStateBlue

|

Sat Mar-25-06 06:48 PM Response to Original message |

| 6. Northern NJ is really sucking wind! |

| Printer Friendly | Permalink | | Top |

| jwirr

|

Sat Mar-25-06 07:09 PM Response to Original message |

| 7. Oh there is a market - many of us would like to own our own |

| Printer Friendly | Permalink | | Top |

| Bush_Eats_Beef

|

Sat Mar-25-06 08:17 PM Response to Original message |

| 15. Median home price in Silicon Valley CA is still $750K... |

| Printer Friendly | Permalink | | Top |

| bedpanartist

|

Sat Mar-25-06 09:06 PM Response to Reply #15 |

| 19. My hometown is fucking apocalyptic |

| Printer Friendly | Permalink | | Top |

| Neil Lisst

|

Sat Mar-25-06 09:05 PM Response to Original message |

| 18. As always, I agree with almost everything you write. |

| Printer Friendly | Permalink | | Top |

| Capn Sunshine

|

Sat Mar-25-06 10:13 PM Response to Original message |

| 21. Gee, that's funny, in California new housing sales in 2/06 are UP 9.5% |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sun Mar-26-06 12:12 AM Response to Reply #21 |

| 24. Southern California |

| Printer Friendly | Permalink | | Top |

| hippiechick

|

Sat Mar-25-06 10:46 PM Response to Original message |

| 22. Median Price $230k ??? JEBUS !! |

| Printer Friendly | Permalink | | Top |

| xkenx

|

Sat Mar-25-06 11:31 PM Response to Original message |

| 23. Flame away, if you will, but |

| Printer Friendly | Permalink | | Top |

| Porcupine

|

Sun Mar-26-06 01:19 AM Response to Reply #23 |

| 26. Housing REPLACED the stock market as a sink for excess capitol |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sun Mar-26-06 03:32 AM Response to Reply #26 |

| 27. Empty Housing Stock |

| Printer Friendly | Permalink | | Top |

| Neil Lisst

|

Sun Mar-26-06 08:48 AM Response to Reply #27 |

| 30. I'm aware of a house just purchased in west Houston |

| Printer Friendly | Permalink | | Top |

| Neil Lisst

|

Sun Mar-26-06 08:40 AM Response to Reply #23 |

| 29. Sorry, but the fluctuations in real estate are as wild as the stock market |

| Printer Friendly | Permalink | | Top |

| joeprogressive

|

Sun Mar-26-06 08:28 AM Response to Original message |

| 28. There are some things going on that point to the big bust |

| Printer Friendly | Permalink | | Top |

| unblock

|

Sun Mar-26-06 10:26 AM Response to Reply #28 |

| 32. "people averaging 10x their salary in housing costs"... this is misleading |

| Printer Friendly | Permalink | | Top |

| spooky3

|

Sun Mar-26-06 11:06 AM Response to Reply #32 |

| 36. don't forget about large down payment effects |

| Printer Friendly | Permalink | | Top |

| unblock

|

Sun Mar-26-06 11:11 AM Response to Reply #36 |

| 37. except that that's not a risk factor |

| Printer Friendly | Permalink | | Top |

| spooky3

|

Sun Mar-26-06 01:24 PM Response to Reply #37 |

| 38. that was not my argument |

| Printer Friendly | Permalink | | Top |

| joeprogressive

|

Sun Mar-26-06 11:55 PM Response to Reply #32 |

| 43. Maybe but there are other indicators that prove my point. |

| Printer Friendly | Permalink | | Top |

| joeprogressive

|

Mon Mar-27-06 12:00 AM Response to Reply #32 |

| 44. "the median house price in palo alto is 10x the median income in palo alto |

| Printer Friendly | Permalink | | Top |

| unblock

|

Mon Mar-27-06 12:42 AM Response to Reply #44 |

| 46. my point is not so much median vs. mean as relevant population |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Wed Mar-29-06 04:35 PM Response to Reply #28 |

| 47. General Rules |

| Printer Friendly | Permalink | | Top |

| AndyA

|

Sun Mar-26-06 10:30 AM Response to Original message |

| 33. America's "Roman Holiday" is about to end |

| Printer Friendly | Permalink | | Top |

| gizmo1979

|

Sun Mar-26-06 10:33 AM Response to Original message |

| 34. You don't have to tell me. |

| Printer Friendly | Permalink | | Top |

| ms liberty

|

Sun Mar-26-06 10:37 AM Response to Original message |

| 35. Reading this, and all the prior comments... |

| Printer Friendly | Permalink | | Top |

| unlawflcombatnt

|

Sun Mar-26-06 04:58 PM Response to Reply #35 |

| 42. North Carolina |

| Printer Friendly | Permalink | | Top |

| earth mom

|

Sun Mar-26-06 02:31 PM Response to Original message |

| 40. K & R! nt |

| Printer Friendly | Permalink | | Top |

| redacted

|

Mon Mar-27-06 12:10 AM Response to Original message |

| 45. The house for sale across the street from us: |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Sun May 05th 2024, 09:27 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion: Presidential (Through Nov 2009) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC