| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

| Home » Discuss » Topic Forums » Economy |

|

| dixiegrrrrl

|

Sat Oct-16-10 09:50 PM Original message |

| The other shoe dropped: TBTF banks sued over mortgage-backed securities. |

| Refresh | +18 Recommendations | Printer Friendly | Permalink | Reply | Top |

| AC_Mem

|

Sat Oct-16-10 09:57 PM Response to Original message |

| 1. Can someone please explain |

| Printer Friendly | Permalink | Reply | Top |

| Lasher

|

Sat Oct-16-10 10:06 PM Response to Reply #1 |

| 2. Sure. |

| Printer Friendly | Permalink | Reply | Top |

| mistertrickster

|

Sat Oct-16-10 10:25 PM Response to Reply #2 |

| 3. Yup . . . that pretty much sums it up. If foreclosed homes don't have a clear title, |

| Printer Friendly | Permalink | Reply | Top |

| dixiegrrrrl

|

Sat Oct-16-10 11:10 PM Response to Reply #3 |

| 11. Some title companies are refusing to insure foreclosed houses. |

| Printer Friendly | Permalink | Reply | Top |

| jtuck004

|

Sun Oct-17-10 03:17 AM Response to Reply #11 |

| 20. And so this drags on, houses can't be sold, it all piles up, |

| Printer Friendly | Permalink | Reply | Top |

| Angry Dragon

|

Sat Oct-16-10 10:25 PM Response to Reply #2 |

| 4. I know it is not funny ......... but your post made me laugh |

| Printer Friendly | Permalink | Reply | Top |

| AC_Mem

|

Sat Oct-16-10 10:45 PM Response to Reply #4 |

| 8. Well, it wasn't meant to be funny... |

| Printer Friendly | Permalink | Reply | Top |

| Angry Dragon

|

Sat Oct-16-10 11:05 PM Response to Reply #8 |

| 10. Your's was not a funny question at all |

| Printer Friendly | Permalink | Reply | Top |

| AC_Mem

|

Sat Oct-16-10 11:23 PM Response to Reply #10 |

| 14. Oh I beg your pardon! |

| Printer Friendly | Permalink | Reply | Top |

| Angry Dragon

|

Sat Oct-16-10 11:32 PM Response to Reply #14 |

| 16. Not a problem |

| Printer Friendly | Permalink | Reply | Top |

| dixiegrrrrl

|

Sat Oct-16-10 11:16 PM Response to Reply #8 |

| 12. It has the strong potential to wipe out the banks. |

| Printer Friendly | Permalink | Reply | Top |

| Lasher

|

Sun Oct-17-10 08:34 AM Response to Reply #4 |

| 23. Gallows humor is fine. |

| Printer Friendly | Permalink | Reply | Top |

| msongs

|

Sat Oct-16-10 11:20 PM Response to Reply #2 |

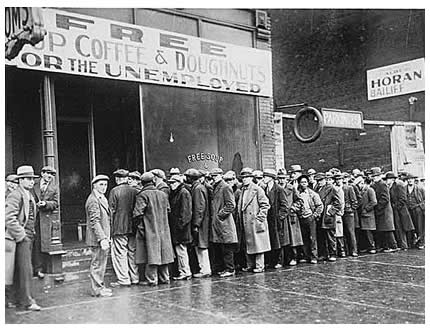

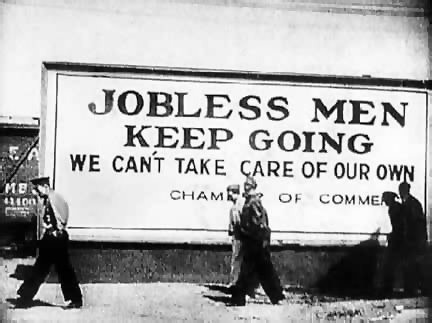

| 13. look at your pic...it's the CHAMBER of COMMERCE! was this taken today? nt |

| Printer Friendly | Permalink | Reply | Top |

| Lasher

|

Sun Oct-17-10 08:25 AM Response to Reply #13 |

| 22. What has been will be again |

| Printer Friendly | Permalink | Reply | Top |

| 704wipes

|

Sat Oct-16-10 11:29 PM Response to Reply #2 |

| 15. I saw a construction site this afternoon that had a sign saying |

| Printer Friendly | Permalink | Reply | Top |

| upi402

|

Mon Oct-18-10 12:15 AM Response to Reply #15 |

| 27. I worked on a job behind one of those signs |

| Printer Friendly | Permalink | Reply | Top |

| iamtechus

|

Sat Oct-16-10 10:27 PM Response to Reply #1 |

| 6. My wife just asked a similar question. |

| Printer Friendly | Permalink | Reply | Top |

| Name removed

|

Sun Oct-17-10 02:25 AM Response to Reply #1 |

| 18. Deleted message |

| jtuck004

|

Sun Oct-17-10 03:12 AM Response to Reply #18 |

| 19. Thank you for posting that. I notice you are new here, so a couple things. |

| Printer Friendly | Permalink | Reply | Top |

| dgibby

|

Sun Oct-17-10 08:50 AM Response to Reply #1 |

| 24. This affects everyone. |

| Printer Friendly | Permalink | Reply | Top |

| Po_d Mainiac

|

Sun Oct-17-10 12:58 PM Response to Reply #1 |

| 25. look at my post #17 n/t |

| Printer Friendly | Permalink | Reply | Top |

| mistertrickster

|

Sat Oct-16-10 10:26 PM Response to Original message |

| 5. I wonder how the idiot Fox-watching CONs are going to blame Barney Frank and Fannie Mae for this. nt |

| Printer Friendly | Permalink | Reply | Top |

| CC

|

Sat Oct-16-10 10:50 PM Response to Reply #5 |

| 9. They will find a way and their veiwers will |

| Printer Friendly | Permalink | Reply | Top |

| Angry Dragon

|

Sat Oct-16-10 10:28 PM Response to Original message |

| 7. Time for Congress to pass a law and stop all bank bonuses |

| Printer Friendly | Permalink | Reply | Top |

| westerebus

|

Sun Oct-17-10 04:18 AM Response to Reply #7 |

| 21. Cat's a pretty good typist. n/t |

| Printer Friendly | Permalink | Reply | Top |

| Po_d Mainiac

|

Sat Oct-16-10 11:35 PM Response to Original message |

| 17. This is a composit of different posts I've written over the last week |

| Printer Friendly | Permalink | Reply | Top |

| upi402

|

Mon Oct-18-10 12:35 AM Response to Reply #17 |

| 28. Larry Hagman Wins $11M from Citi in Securities Arbitration |

| Printer Friendly | Permalink | Reply | Top |

| AtheistCrusader

|

Sun Oct-17-10 07:38 PM Response to Original message |

| 26. How many shoes is this monster wearing? |

| Printer Friendly | Permalink | Reply | Top |

| DU

AdBot (1000+ posts) |

Sun May 05th 2024, 04:35 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Topic Forums » Economy |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC