Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Economy

In reply to the discussion: STOCK MARKET WATCH - Tuesday, 17 January 2012 [View all]Demeter

(85,373 posts)37. S&P versus ECB

http://www.macrobusiness.com.au/2012/01/sp-versus-ecb/

Last night we saw the first salvo in a long war between the rating agencies and the ECB’s emergency action to prevent total European financial melt-down. The ECB came out on top, with France selling 1.9 billion euros of one-year notes today at a yield of 0.406 percent, down from 0.454 percent. The European equities market received the news well and jumped on the result. Given the recent sub-3 year issuance results this wasn’t really a surprise, but it did provide some much needed good news.

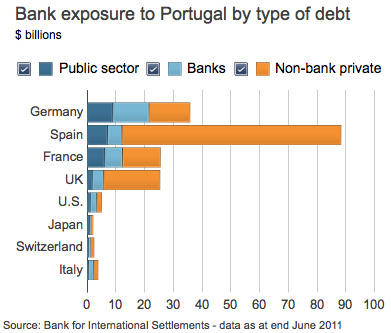

Although the market appears to have taken the downgrade of France in its stride, the junking of Portugal is a different matter. The Portuguese 10yr yield jumped 15.6% overnight. This result isn’t an immediate issue given the fact that the country is already on life support, but the result is likely to be yet another hit to the banking sector, specifically German and Spanish banks from the looks of recent data:

It would appear that Portugal is slowly slipping in the direction of Greece. The latest report from the country’s central bank certainly isn’t happy reading:

Yields on Spanish and Italian bonds hardly moved overnight suggesting that the ECB’s SMP program was once again busy. The ECB was very active last week with €3.77bn in sovereign purchases, up from €1.1bn the week before. That is the highest level of activity for 3 months and I see no reason to suggest that pace will slow.

After the market closed S&P released yet another well-choreographed salvo on Europe with the downgrade of the EFSF:

And then the return fire from the ECB:

There is no doubt that these ratings were already priced in by the markets. There have been rumours circulating about the downgrade of France for over a month and even the French finance minister had stated that it would be a miracle if France was able to keep the top rating. What I don’t think has been priced in by the markets, as I discussed yesterday, is S&P’s negative outlook based on the continuation of the current policies. As far a I can tell, the response from the European leadership thus far has been to re-state their commitment to the “fiscal compact” with a few addition motherhood statements about “focussing on growth”. The problem is that most of what S&P warned about in their ratings assessment is the exact plan Europe currently has for itself.

Mario Draghi may consider the rating agencies to be irrelevant but the big swing in the Portuguese yields suggest many others don’t share his view and the problem for the European banks is that , at this stage, neither does the ECB’s operating procedure:

Although markets had already anticipated the moves by the rating agencies, I am very doubtful they have priced in what is happening in Greece.

Greece sent senior officials to Washington on Monday for meetings with the International Monetary Fund (IMF) as it raced against the clock to break a deadlock in debt swap talks that has prompted new fears of an unruly default.

Barely a month after an injection of bailout funds helped avert bankruptcy, Greece is back at the centre of the eurozone crisis as fears of a default and a subsequent eurozone exit overshadow a mass credit downgrade of eurozone countries.

Athens needs a deal with the private sector within days to avoid going bankrupt when €14.5bn of bond redemptions fall due in late March. But talks with its creditor banks broke down without an agreement on Friday.

…

Charles Dallara, head of the Institute of International Finance who represents Greece’s private creditors, told the Financial Times an agreement in principle was needed by the end of this week if it was to be finalised in time for the March bond redemptions. He said the Greeks were not the problem.

“All the European heads of state said they wanted a deal with a 50% (haircut) and a voluntary agreement,” Dallara was quoted as saying. “Some of their own collaborators are not following that decision.”

After initial optimism last week that a deal was near, negotiations stalled on Friday over the interest rate Greece must pay on new bonds it offers.

One banking source said official sector creditors had asked for a coupon of less than 4%, irking banks for whom it would have meant losses of over 75% on the bonds.

A second source said the banks were ready to strike a deal if they reached common ground with the EU, IMF and ECB.

German and French officials have now been called in to help break the deadlock between parties. The disagreement appears to be focussed on what coupon will be paid on a 30 year bond and also the involvement of non-private parties. Greece faces a €14.4bn redemption payment in March and needs to have the second bailout programme in place to avoid a default. I have long stated that Greece will eventually default. Even if this deal does get through and Greece eventually gets yet another bailout I doubt it will be too long before Greece is back at the negotiating table asking once again for additional funds. Supposedly Greece has just 45 days to avoid default....

Last night we saw the first salvo in a long war between the rating agencies and the ECB’s emergency action to prevent total European financial melt-down. The ECB came out on top, with France selling 1.9 billion euros of one-year notes today at a yield of 0.406 percent, down from 0.454 percent. The European equities market received the news well and jumped on the result. Given the recent sub-3 year issuance results this wasn’t really a surprise, but it did provide some much needed good news.

Although the market appears to have taken the downgrade of France in its stride, the junking of Portugal is a different matter. The Portuguese 10yr yield jumped 15.6% overnight. This result isn’t an immediate issue given the fact that the country is already on life support, but the result is likely to be yet another hit to the banking sector, specifically German and Spanish banks from the looks of recent data:

It would appear that Portugal is slowly slipping in the direction of Greece. The latest report from the country’s central bank certainly isn’t happy reading:

The forecasts released Tuesday by the Portuguese central bank are the gloomiest to date and predict a worrying contraction for the Portuguese economy: 2012 should register a 3.1% contraction from the 2.2% forecast just three months ago. The scenario is described in the Bank of Portugal’s winter bulletin released today as ”an unprecedented contraction of the Portuguese economic activity“, brought on by austerity measures and the growing uncertainty surrounding the crisis in the eurozone.

The Portuguese central bank forecasts a 3.1% contraction in 2012 and a virtual stagnation in 2013, when the country’s economy should grow just 0.3%. However, the forecasts for 2011 were revised slightly upward, to 1.6% from last October’s forecast of a 1.9% fall.

Internal demand, the main driver of next year’s contraction, also registered a significant worsening in the central bank’s winter bulletin. The Bank of Portugal is now expecting a 6.5% fall from the 4.8% contraction forecast for 2012, as the country is in the grip of a huge austerity drive which has brought on an overall increase in prices, tax hikes, and cuts to wages and benefits as part of the government’s policies, as it strives to comply with the €78bn bailout agreement signed with the European Central Bank, the International Monetary Fund and the European Commission, in 2011.

The Portuguese central bank forecasts a 3.1% contraction in 2012 and a virtual stagnation in 2013, when the country’s economy should grow just 0.3%. However, the forecasts for 2011 were revised slightly upward, to 1.6% from last October’s forecast of a 1.9% fall.

Internal demand, the main driver of next year’s contraction, also registered a significant worsening in the central bank’s winter bulletin. The Bank of Portugal is now expecting a 6.5% fall from the 4.8% contraction forecast for 2012, as the country is in the grip of a huge austerity drive which has brought on an overall increase in prices, tax hikes, and cuts to wages and benefits as part of the government’s policies, as it strives to comply with the €78bn bailout agreement signed with the European Central Bank, the International Monetary Fund and the European Commission, in 2011.

Yields on Spanish and Italian bonds hardly moved overnight suggesting that the ECB’s SMP program was once again busy. The ECB was very active last week with €3.77bn in sovereign purchases, up from €1.1bn the week before. That is the highest level of activity for 3 months and I see no reason to suggest that pace will slow.

After the market closed S&P released yet another well-choreographed salvo on Europe with the downgrade of the EFSF:

The European Financial Stability Facility lost its top credit rating at Standard & Poor’s after the rating company downgraded France and Austria.

The rating was lowered to AA+ from AAA, S&P said in a statement today. It had said on Dec. 6 that the loss of an AAA rating by any one of the EFSF’s guarantor nations may lead to the facility being downgraded.

“The EFSF’s obligations are no longer fully supported either by guarantees from EFSF members rated AAA by S&P, or by AAA rated securities,” the company said. “Credit enhancements sufficient to offset what we view as the reduced creditworthiness of guarantors are currently not in place.”

S&P removed the ratings on the facility from CreditWatch with negative implications, it also said.

The rating was lowered to AA+ from AAA, S&P said in a statement today. It had said on Dec. 6 that the loss of an AAA rating by any one of the EFSF’s guarantor nations may lead to the facility being downgraded.

“The EFSF’s obligations are no longer fully supported either by guarantees from EFSF members rated AAA by S&P, or by AAA rated securities,” the company said. “Credit enhancements sufficient to offset what we view as the reduced creditworthiness of guarantors are currently not in place.”

S&P removed the ratings on the facility from CreditWatch with negative implications, it also said.

And then the return fire from the ECB:

European Central Bank chief Mario Draghi on Monday downplayed the importance of ratings agencies after Standard & Poor’s mass downgrade of eurozone countries, saying markets had priced in the action.

“I think what we should do is to learn either to do without them or with them but to a much more limited way than we do today,” said Draghi, in his capacity as head of the European Systemic Risk Board (ESRB).

“To a great extent, markets anticipated these ratings changes and priced their assets as if these ratings had already been issued,” said Draghi, speaking at the European Parliament in Strasbourg.

“I think what we should do is to learn either to do without them or with them but to a much more limited way than we do today,” said Draghi, in his capacity as head of the European Systemic Risk Board (ESRB).

“To a great extent, markets anticipated these ratings changes and priced their assets as if these ratings had already been issued,” said Draghi, speaking at the European Parliament in Strasbourg.

There is no doubt that these ratings were already priced in by the markets. There have been rumours circulating about the downgrade of France for over a month and even the French finance minister had stated that it would be a miracle if France was able to keep the top rating. What I don’t think has been priced in by the markets, as I discussed yesterday, is S&P’s negative outlook based on the continuation of the current policies. As far a I can tell, the response from the European leadership thus far has been to re-state their commitment to the “fiscal compact” with a few addition motherhood statements about “focussing on growth”. The problem is that most of what S&P warned about in their ratings assessment is the exact plan Europe currently has for itself.

Mario Draghi may consider the rating agencies to be irrelevant but the big swing in the Portuguese yields suggest many others don’t share his view and the problem for the European banks is that , at this stage, neither does the ECB’s operating procedure:

Italian banks need additional collateral to obtain funding after the country’s credit rating was cut by Standard & Poor’s and the London Clearing House raised its margin calls on Italian bonds, Deutsche Bank AG (DBK) said.

“These points are negative for the Italian banks, for the pressure on their sovereign holdings and on interbanking funding,” Paola Sabbione, a Milan-based analyst at Deutsche Bank, said in a note to investors. “A larger collateral is now required to obtain the same ECB funding.”

“These points are negative for the Italian banks, for the pressure on their sovereign holdings and on interbanking funding,” Paola Sabbione, a Milan-based analyst at Deutsche Bank, said in a note to investors. “A larger collateral is now required to obtain the same ECB funding.”

Although markets had already anticipated the moves by the rating agencies, I am very doubtful they have priced in what is happening in Greece.

Greece sent senior officials to Washington on Monday for meetings with the International Monetary Fund (IMF) as it raced against the clock to break a deadlock in debt swap talks that has prompted new fears of an unruly default.

Barely a month after an injection of bailout funds helped avert bankruptcy, Greece is back at the centre of the eurozone crisis as fears of a default and a subsequent eurozone exit overshadow a mass credit downgrade of eurozone countries.

Athens needs a deal with the private sector within days to avoid going bankrupt when €14.5bn of bond redemptions fall due in late March. But talks with its creditor banks broke down without an agreement on Friday.

…

Charles Dallara, head of the Institute of International Finance who represents Greece’s private creditors, told the Financial Times an agreement in principle was needed by the end of this week if it was to be finalised in time for the March bond redemptions. He said the Greeks were not the problem.

“All the European heads of state said they wanted a deal with a 50% (haircut) and a voluntary agreement,” Dallara was quoted as saying. “Some of their own collaborators are not following that decision.”

After initial optimism last week that a deal was near, negotiations stalled on Friday over the interest rate Greece must pay on new bonds it offers.

One banking source said official sector creditors had asked for a coupon of less than 4%, irking banks for whom it would have meant losses of over 75% on the bonds.

A second source said the banks were ready to strike a deal if they reached common ground with the EU, IMF and ECB.

German and French officials have now been called in to help break the deadlock between parties. The disagreement appears to be focussed on what coupon will be paid on a 30 year bond and also the involvement of non-private parties. Greece faces a €14.4bn redemption payment in March and needs to have the second bailout programme in place to avoid a default. I have long stated that Greece will eventually default. Even if this deal does get through and Greece eventually gets yet another bailout I doubt it will be too long before Greece is back at the negotiating table asking once again for additional funds. Supposedly Greece has just 45 days to avoid default....

Edit history

Please sign in to view edit histories.

78 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

"If President Obama is serious about saving the middle class and reducing income inequality..."

jtuck004

Jan 2012

#11

Second MF Global Unveiled As Canadian Regulator Accuses Barret Capital Of Commingling Client Funds

DemReadingDU

Jan 2012

#50