TomCADem

TomCADem's JournalNew Yorker - "Obamacares Three Per Cent" Or, Catastrophic Health Plans...

...are not really health coverage. The MSM has been pushing a false equivalency between individual catastrophic health plans and coverage that individuals are required to obtain under the ACA. The media simply says, "Hey, look someone must replace their coverage." Yet, the real story is that they really weren't receiving health care coverage.

http://www.newyorker.com/online/blogs/newsdesk/2013/10/obamacares-three-per-cent.html?mobify=0

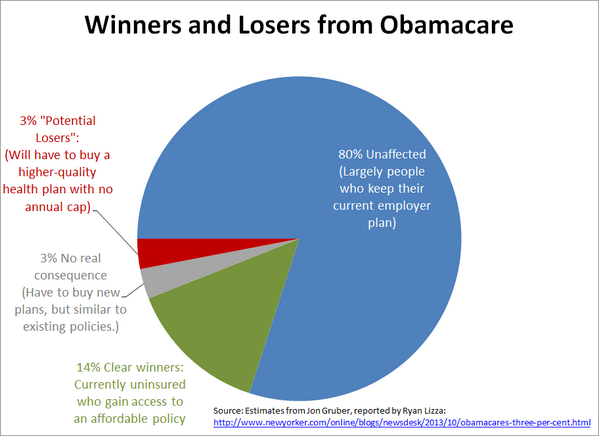

Gruber broke down the A.C.A. “winners” and “losers” for me. About eighty per cent of Americans are more or less left alone by the health-care act—largely people who have health insurance through their employers. About fourteen per cent of Americans are clear winners: they are currently uninsured and will have access to an affordable insurance policy under the A.C.A.

But much of the current controversy involves the six per cent of Americans who buy their own health care on the individual market, which the A.C.A. has dramatically reformed. Gruber argued that half of these people (three per cent of all Americans) will have little change to their polices. “They have to buy new plans, but they will be pretty similar to what they had before,” he said. “It will essentially be relabeling.”

The other half, however, also three per cent of the population, will have to buy a new product that complies with the A.C.A.’s more stringent requirements for individual plans. A significant portion of these roughly nine million Americans will be forced to buy a new insurance policy with higher premiums than they currently pay. The primary reason for the increased cost is that the A.C.A. bans any plan that would require a people who get sick to pay medical fees greater than six thousand dollars per year. In other words, this was a deliberate policy decision that the White House and Congress made to raise the quality—and thus the premiums—of insurance policies at the bottom end of the individual market.

“We’ve decided as a society that we don’t want people to have insurance plans that expose them to more than six thousand dollars in out-of-pocket expenses,” Gruber said. Obama obviously should have known that his blanket statement about “keeping what you have” could not apply to this class of policyholders.

Slate - "The Chart That Could Save Obamacare" - Or, Death Panels II

Here is a nice story that illustrates how the MSM continues to enable the right by pushing a false equivalency between the relatively few people who are worse off under the ACA versus those who are tremendously benefitted. Rather than provide proportional coverage to those who would be better off, the MSM actually focuses on those who claim they are worse off. Yet, as this story illustrates, those who claim they are worse off often aren't.

http://www.slate.com/blogs/weigel/2013/10/31/the_chart_that_could_save_obamacare.html

Seems right to me; it so happens that the 6 percent of humans likely to lose their plans and pay more constitute millions of Americans, and that even a small number of them can talk to the media about how horrid the experience is. What they need is a long trench warfare campaign of fact-checking and, occasionally, apologizing. Michael Hiltzik, for example, has reported out the tale of Deborah Cavallaro, a Los Angeles woman spiriting around conservative-leaning shows to explain how Obamacare killed her plan.Her current plan, from Anthem Blue Cross, is a catastrophic coverage plan for which she pays $293 a month as an individual policyholder. It requires her to pay a deductible of $5,000 a year and limits her out-of-pocket costs to $8,500 a year. Her plan also limits her to two doctor visits a year, for which she shoulders a copay of $40 each. After that, she pays the whole cost of subsequent visits... at her age, she's eligible for a good "silver" plan for $333 a month after the subsidy -- $40 a month more than she's paying now. But the plan is much better than her current plan -- the deductible is $2,000, not $5,000. The maximum out-of-pocket expense is $6,350, not $8,500. Her co-pays would be $45 for a primary care visit and $65 for a specialty visit -- but all visits would be covered, not just two.

Is that better than her current plan? Yes, by a mile.

But cutting through the fog of the Cavallaro story took several days, and she's going to have a lot of company.

Profile Information

Member since: Fri May 8, 2009, 12:59 AMNumber of posts: 17,390